What is the formula for cash collected from customers?

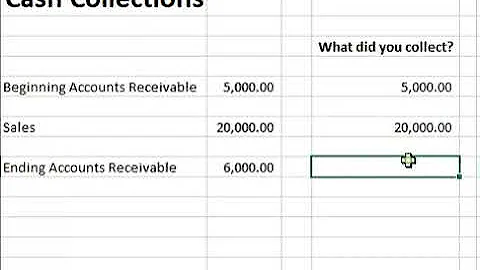

The cash collections formula calculates the actual cash a business receives from its customers. It's determined by adding the starting accounts receivable to the earned revenue and then subtracting the ending accounts receivable.

- Cash Collections = (Beginning Accounts Receivable + Credit Sales) – Ending Accounts Receivable.

- Beginning Accounts Receivable: This is the accounts receivable balance at the beginning of the period.

- Credit Sales: This represents the total amount of sales made on credit during the period.

Cash Collected From Customers is the amount received in cash related to goods or services performed to customers. This includes collection from cash sales and sales on account for the period. Collection from sales on account can be determined using the changes in balance of accounts receivable for the period.

The cash collections equation

To calculate your total expected cash collections, you'll add the revenue you anticipate will come from cash sales to the revenue you anticipate will come from accounts receivable. You can estimate cash sales from the year's previous trends.

Important cash flow formulas to know about:

Free Cash Flow = Net income + Depreciation/Amortization – Change in Working Capital – Capital Expenditure. Operating Cash Flow = Operating Income + Depreciation – Taxes + Change in Working Capital.

Calculate the expected cash collections for the current period by multiplying the total sales made during this period by the collection percentage. Find the uncollected amount from last month's credit sales.

Cash collections refers to the total amount of payments collected from customers in exchange for goods and services. It can be calculated by adding your cash sales with the estimated collections from accounts receivable.

- Cash Received from Customers = Sales + Decrease (or - Increase) in Accounts Receivable.

- Cash Paid to Suppliers = Cost of Goods Sold + Increase (or - Decrease) in Inventory + Decrease (or - Increase) in Accounts Payable.

| Basis | Cash received from customers |

|---|---|

| Meaning | The cash received is the amount which is collected by the company on credit sale of goods from the customer |

| Accounting treatment | The cash received is treated as income from the sale as well as liability if the cash received from the customer is an advance |

Cash sales = Net Sales – Credit Sales + Sales Return.

What is the formula for cash earnings?

Cash EPS = Operating Cash Flow / Diluted Shares Outstanding

For example, depreciation expense is deducted from net income but does not actually involve any outflow of cash. Thus, this must be added back to net income to remove the accounting impact. Note: Cash EPS is different from Diluted EPS.

Formula for Cash Available for Distribution (CAD)

Calculating cash available for distribution is done by subtracting recurring capital expenditures from funds from operations.

The formula for calculating cash balance is: Cash balance = beginning cash balance + cash inflows – cash outflows. When trying to calculate your cash balance, it's important to start with the basics. Your cash balance is the amount of money you have in your accounts at any given time.

To calculate the amount of cash collected from the customers add receivable at the beginning to the sales revenue and deduct receivables at the ending.

Cash collection refers to the activities and processes involved in collecting cash payments from customers for goods and services provided by a business. The collection of funds is a fundamental aspect of cash flow management.

The cash collection formula is straightforward: Total Cash Collections = Beginning Receivables + Sales - Ending Receivables.

Average Collection Period = 365 Days * (Average Accounts Receivables / Net Credit Sales) Alternatively and more commonly, the average collection period is denoted as the number of days of a period divided by the receivables turnover ratio. The formula below is also used referred to as the days sales receivable ratio.

Calculate Total Expected Collections: Sum up the immediate cash sales, the scheduled collections from credit sales based on the credit terms, and the collections on pre-existing receivables to get the total expected cash collections.

First, multiply the average accounts receivable by the number of days in the period. Divide the sum by the net credit sales. The resulting number is the average number of days it takes you to collect an account.

1. Cash receipts from customers = Revenue from operations + Trade receivables in the beginning – Trade receivables in the end. 2. Cash payments to suppliers = Purchases + Trade Payables in the beginning – Trade Payables in the end.

How do you record cash collected from customers?

Record your cash sales in your sales journal as a credit and in your cash receipts journal as a debit. Keep in mind that your entries will vary if you offer store credit or if customers use a combination of payment methods (e.g., part cash and credit).

- Net Cash-Flow = Total Cash Inflows – Total Cash Outflows.

- Net Cash Flow = Operating Cash Flow + Cash Flow from Financial Activities (Net) + Cash Flow from Investing Activities (Net)

- Operating Cash Flow = Net Income + Non-Cash Expenses – Change in Working Capital.

To calculate the cash received from customers in Case X, add the sales to the opening account receivable and then subtract the closing account receivable.

Accounts receivable (AR) are funds the company expects to receive from customers and partners. AR is listed as a current asset on the balance sheet.

A cash flow statement is a key financial statement that records the amount of cash that comes into and goes out of a company over a specific period. The cash flow statement records where a company's money is coming from and where it's going over a specific period.