What is the 10 rule for saving money?

The 10% rule is a savings tip that suggests you set aside 10% of your gross monthly income for retirement or emergencies. If you still need to start a savings account, this is a great way to build up your savings. You should create a monthly budget before starting your savings journey.

The 10% savings rule is very simple. It states you should save 10% of everything you earn. If you earn $3,000 per month, you save $300.

By allocating 70% for what you need, 20% for what you want (either immediate luxuries or future savings goals), and 10% for your goals (like paying off debts and saving or investing in your future), you can work towards a greater sense of financial wellbeing.

The most common way to use the 40-30-20-10 rule is to assign 40% of your income — after taxes — to necessities such as food and housing, 30% to discretionary spending, 20% to savings or paying off debt and 10% to charitable giving or meeting financial goals.

The rule is simple: spend less than you earn. The basic idea behind the Golden Rule of Spending is that you should always spend less than you earn. This means that you should only spend what you make in income, and you should be careful to budget your money in a way that allows you to save and invest for the future.

The 40/40/20 rule comes in during the saving phase of his wealth creation formula. Cardone says that from your gross income, 40% should be set aside for taxes, 40% should be saved, and you should live off of the remaining 20%.

The seven percent savings rule provides a simple yet powerful guideline—save seven percent of your gross income before any taxes or other deductions come out of your paycheck. Saving at this level can help you make continuous progress towards your financial goals through the inevitable ups and downs of life.

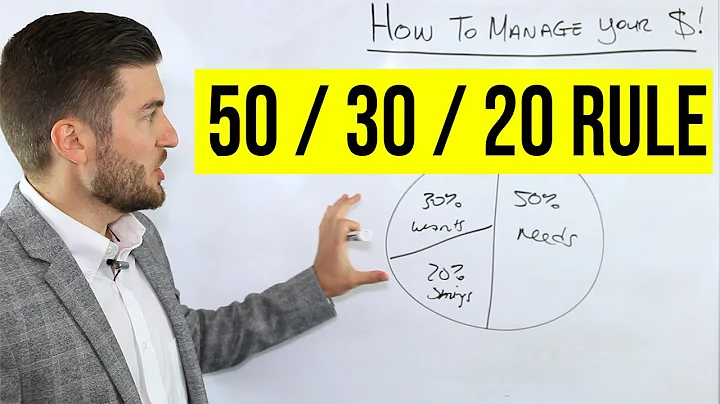

The 50-30-20 rule recommends putting 50% of your money toward needs, 30% toward wants, and 20% toward savings. The savings category also includes money you will need to realize your future goals. Let's take a closer look at each category.

Poorman suggests the popular 50/30/20 rule of thumb for paycheck allocation: 50% of net pay for essentials: groceries, bills, rent or mortgage, debt payments, and insurance. 30% for spending on dining or ordering out and entertainment. 20% for personal saving and investment goals.

The basic rule of thumb is to divide your monthly after-tax income into three spending categories: 50% for needs, 30% for wants and 20% for savings or paying off debt.

What is Rule 69 in finance?

What is the Rule of 69? The Rule of 69 is used to estimate the amount of time it will take for an investment to double, assuming continuously compounded interest. The calculation is to divide 69 by the rate of return for an investment and then add 0.35 to the result.

When following the 10-10-80 rule, you take your income and divide it into three parts: 10% goes into your savings, and the other 10% is given away, either as charitable donations or to help others. The remaining 80% is yours to live on, and you can spend it on bills, groceries, Netflix subscriptions, etc.

The 80/20 rule says that you should first set aside 20% of your net income for saving and paying down debt. Then split up the additional 80% between needs and wants.

It's an easy way to calculate just how long it's going to take for your money to double. Just take the number 72 and divide it by the interest rate you hope to earn. That number gives you the approximate number of years it will take for your investment to double.

The idea is to divide your income into three categories, spending 50% on needs, 30% on wants, and 20% on savings. Learn more about the 50/30/20 budget rule and if it's right for you.

If you find yourself in this situation, consider the “Rule of Three:” When you have an unexpected windfall, put 1/3 of the windfall towards paying down debt, 1/3 towards long-term saving and investing, and the remaining 1/3 towards something rewarding or fun. Let's take each in turn and talk about the benefits.

Personal finance expert Dave Ramsey says if you're going through a tough financial period, you should budget for the “Four Walls” first above anything else. In a series of tweets, Ramsey suggested budgeting for food, utilities, shelter and transportation — in that specific order.

Yes, a 401(k) can count as savings in a 50/30/20 budget plan. But if 401(k) contributions are automatically deducted from your paycheck, they're not included in your take-home pay calculation.

The 30% Rule Is Outdated

Rather than looking at what consumers should be spending on housing, however, the government selected these percentages because that's what consumers were spending.

1 At 10%, you could double your initial investment every seven years (72 divided by 10). In a less-risky investment such as bonds, which have averaged a return of about 5% to 6% over the same period, you could expect to double your money in about 12 years (72 divided by 6).

Which behavior can help increase savings?

Reduce Discretionary Spending. If you are trying to increase your monthly savings, the most effective way is to reduce discretionary expenditures. These are purchases that you may enjoy but are not necessary. This way, you can add that dollar amount to your automatic monthly transfer into your savings account!

The 50/30/20 budget rule states that you should spend up to 50% of your after-tax income on needs and obligations that you must have or must do. The remaining half should be split between savings and debt repayment (20%) and everything else that you might want (30%).

- Budgeting Mistake #1: Not Saving for Emergencies. ...

- Budgeting Mistake #2: Overestimating How Much You Have Left to Spend. ...

- Budgeting Mistake #3: Leaving Out Money for Fun.

- Change bank accounts. ...

- Be strategic with your eating habits. ...

- Change up your insurance. ...

- Ask for a raise—or start job hunting. ...

- Consider a side hustle. ...

- Take advantage of a credit card that offers rewards. ...

- Switch up your transportation habits. ...

- Cancel subscriptions you don't really need or use.

The 50/30/20 rule is a streamlined plan for anyone looking to spend and save responsibly. This rule recommends that you spend 50% of your post-tax income on necessities (housing, food, utilities, transportation, insurance, childcare); and 30% on wants (travel, gym memberships, cable, dining out, etc.).